(February 15, 2016)

Bets are rising that Pakistan will default on its debt just as it starts to revive investor interest with a reduction in terrorist attacks.

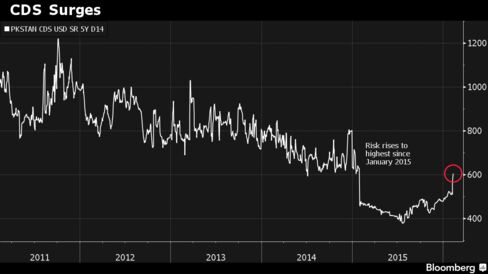

Credit default swaps protecting the nation’s debt against non-payment for five years surged 56 basis points last week to 620 points amid the global market sell-off, according to data compiled by Bloomberg. That’s the highest since January 2015 and the steepest jump after Greece, Venezuela and Portugal among more than 50 sovereigns tracked by Bloomberg.

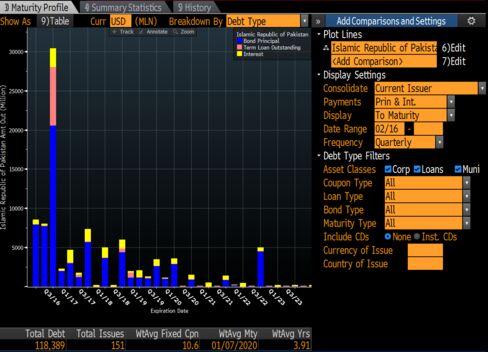

About 40 percent of Pakistan’s outstanding debt — both local and foreign — is due to mature in 2016, according to data compiled by Bloomberg. That’s roughly $45 billion, of which about 4.3 trillion rupees ($41 billion) is in local currency.

Prime Minister Nawaz Sharif has worked to make Pakistan more investor-friendly since winning a $6.6 billion International Monetary Fund loan in 2013 to avert an external payments crisis. The economy is forecast to grow 4.5 percent, an eight-year high, as a crackdown on militant strongholds helps reduce deaths from terrorist attacks.

“Pakistan’s high level of public debt, with a large portion financed through short-term instruments, does make the sovereign’s ability to meet their financing needs more sensitive to market conditions,” Mervyn Tang, lead analyst for Pakistan at Fitch Ratings Ltd., said by e-mail.

Right now, he said, there’s not much reason to panic. Pakistan’s external liabilities are “relatively modest,” foreign-currency reserves have risen, existing IMF funding will help meet maturing loans over the next two years and Chinese investment in an economic corridor is on its way, Tang said.

“Improving growth prospects, lower inflation and smaller budget deficit should help to underpin investor confidence, particularly the domestic investor base,” Tang said.

Pakistan has just $4 billion of external debt coming due in 2016 and “does not face any difficulty in respect of its debt servicing obligations,” the Finance Ministry said on Monday in an e-mailed response to questions. The government doesn’t “feel any cause for concern with regards to refinancing its domestic debt,” it said.

Public debt risk indicators such as short-term debt as share of total obligations have come down over the past two years, the CDS is on a downward trajectory compared with 2008, and Sharif’s administration has successfully tapped the capital markets, the Finance Ministry said. Pakistan has a medium risk of default over five years, according to Bloomberg assessments.

Pakistan is committed to successfully implement its IMF macroeconomic stability program, the Finance Ministry said in a statement Feb. 1. Sharif’s administration has a “quite good” chance of completing the program, IMF mission chief Harald Finger said last month.

Since Sharif took the IMF loan, Pakistan’s debt due by end-2016 has jumped about 79 percent. He’s also facing resistance in meeting IMF demands to privatize state-owned companies, leading to a strike this month at national carrier Pakistan International Airlines Corp.

The bulk of this year’s debt, some 2.4 trillion rupees ($23 billion), is due between July and September, and repayments will get tougher if borrowing costs rise more. The spread between Pakistan’s 10-year sovereign bond and similar-maturity U.S. Treasuries touched a one-year high on Thursday.

If Pakistan’s debt servicing costs rise, Sharif doesn’t have much room to maneuver. Already about 77 percent of the country’s 13 trillion rupees ($124 billion) budget for the year through June 30 is earmarked for interest and principal repayment on loans.

Pakistan’s external requirement accounts for 19 percent of the nation’s $21 billion in foreign-exchange holdings.

That stockpile, however, isn’t airtight. While it increased by more than 55 percent last year — the steepest rise in Asia — more than half consists of debt and grants that could leave the country quickly if global risk appetite worsens. Outflows would weaken the rupee, a currency that is estimated by the IMF to be as much as 20 percent overvaluedeven though it’s proved remarkably stable amid the recent market turmoil.

“The obligations maturing during the year are fully covered by reserves as well as the planned build up during the year,” Ehtasham Rashid, Director General at the Debt Policy Coordination Office of the Finance Ministry, said by e-mail. “It is fallacious to claim that Pakistan has built reserves on the back of short-term borrowings.”

Investors should expect volatility in bonds and pressure on the rupee this year, according to Mustafa Pasha, head of investments at Lakson Investments Ltd., which manages $200 million of Pakistani stocks and bonds.

While the plunge in oil prices helped the government last year, predicting the outlook would be like “reading the tea leaves,” he said by phone from Karachi.

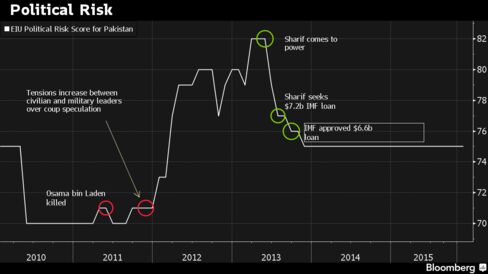

Another worry, as ever in Pakistan, is political stability. The military has ruled the country for most of the time since independence in 1947, and General Raheel Sharif — no relation to the prime minister — has boosted the army’s image with a campaign to root out terrorists who massacred 134 children in 2014.

While Raheel Sharif has said he plans to retire when his term ends in November, the risk of political upheaval is ever present. Pakistan has the 10th highest political risk score among more than 120 countries in the Economist Intelligence Unit ranking, worse than Egypt and Iran.